Under the National Credit Act and its amendments, credit providers are required to perform affordability assessments before granting credit.

In practice, this means reviewing a customer’s bank statement data – either through physical statements, uploaded PDFs, or digital retrieval.

South Africa processes roughly 18 million credit applications per quarter – around 6 million per month.

Today, the aggregation ecosystem supports in the region of ~400,000 secure digital bank data retrievals per month.

That implies that approximately 5.6 million monthly applications still rely on manual or document-based submission of bank statements.

That is the current landscape.

This piece focuses on the digital access layer.

Screen-based retrieval emerged because open APIs were not universally available, while affordability assessments remained mandatory.

It enabled:

- Consumer-permissioned data sharing

- NCA-aligned compliance

- Inclusion for non-bank lenders – levelling the competitive landscape

- Digitised onboarding and faster underwriting

Secure screen-based retrieval currently supports a meaningful portion of South Africa’s digital credit origination volume.

That signals:

- Recurring revenue

- Institutional reliance

- Embeddedness

- Durability

It is commercial infrastructure.

Globally, financial systems are moving toward Open Banking and Open Finance frameworks, where consumers share data via structured APIs.

APIs introduce:

- Tokenised authentication

- Standardised data formats

- Clearer liability allocation

- Cleaner institutional integration

- Improved customer journeys

They represent the next layer of maturity – and the infrastructure required to extend structured digital access beyond the current ~400,000 monthly retrievals toward the broader 6 million monthly credit applications.

A functional open finance framework does not replace what exists today. It scales it.

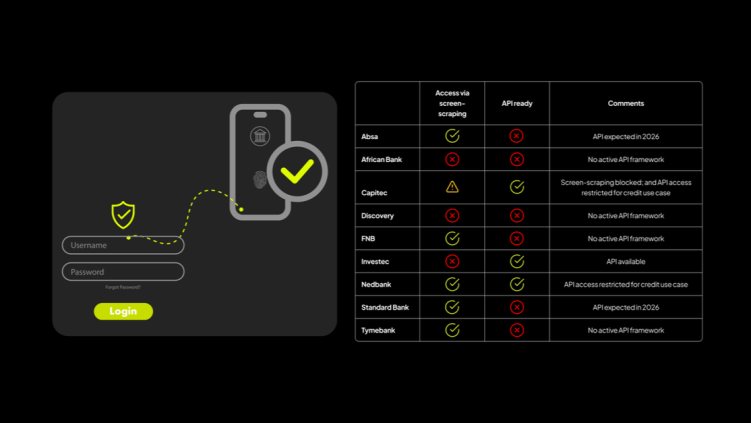

So where does South Africa stand?

The table reflects a mixed environment.

Some banks enable screen-based retrieval. Some provide APIs. Some restrict underwriting use cases. Some operate both models.

We are in a transitional phase, with the Open Finance regulatory timeline still unclear.

Screen-based retrieval supports compliance and credit origination today. APIs will standardise and scale the ecosystem over time.

But access is uneven – and uneven access creates uneven competition.

In our view, the imbalance in data access across institutions makes stronger regulatory supervision increasingly necessary. Innovation depends on it. Financial inclusion depends on it. Consumers depend on it.

Levelling the playing field is not about forcing change. It is about ensuring that infrastructure evolves in a way that supports competition, inclusion, and regulatory compliance.

South Africa needs a safe and structured transition between the two.

Recent regulatory developments – particularly SARB’s Directive 2 of 2024 – reflect a progressive step toward strengthening governance around credential handling and third-party participation within the National Payment System.

While introduced to enhance oversight and system integrity, the Directive also has constructive implications for the future of secure data sharing. Clearer guardrails around access, accountability, and supervision create the conditions required for structured open finance to evolve responsibly.

We have drawn parallels between this regulatory direction and the practical realities of today’s aggregation ecosystem. In response, we published a white paper outlining a safe and commercially workable bridge from secure screen-based retrieval to structured API-based access – making the transition from current infrastructure to open banking more intentional and coordinated.

The foundations already exist.

The priority now is to strengthen them – deliberately, collaboratively, and step by step.